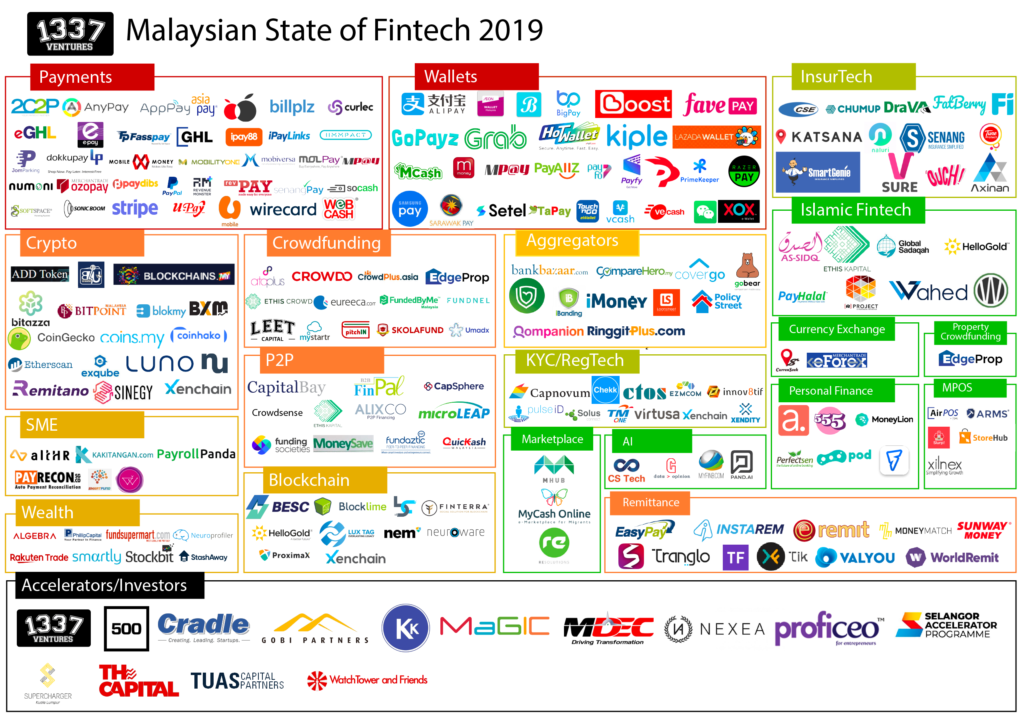

Presenting 1337 Ventures’ comprehensive 2019 list of Fintech Startup Players in Malaysia! Whilst running Bank Negara Malaysia’s Fintech Accelerator – Alpha Startups: MyFintech Week edition, 1337 Ventures was exposed to many fintech startups in the scene: while researching for startups, the state of the industry, problem statements, and new budding ideas. The result? The newly updated Malaysian Fintech Map.

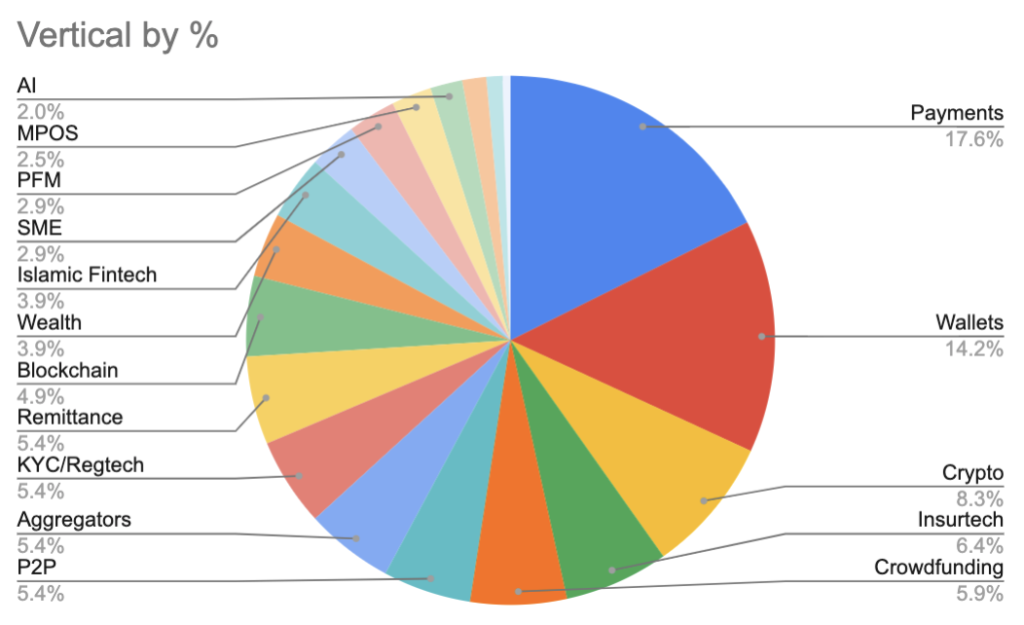

This diagram segments Malaysian Fintech startups into various verticals to give you an eagle’s view of the current state of the Fintech industry in Malaysia. Through this diagram, you can identify the current players in the market in just one glance. For example, from a brief glance, one can see that the “Wallet” and “Payment” verticals are very crowded, compared to verticals such as “AI” or “Personal Finance”.

If you’re interested in entering the Fintech space, do refer to this diagram as a starting point before making any costly decisions. Factor in: who are your competitors? Is your space currently crowded? Who are the major players and partners that you could possibly collaborate with? By curating this list, we hope that it helps you answer these pertinent questions.

For a high resolution of the diagram, do visit here.

Feel free to fill up this form if you know of any fintech startups that are evidently missing here, and share this post if you wish to help grow this collaborative list!

Problem Statements in the Industry

In collaboration with Bank Negara Malaysia, 1337 Ventures collected a list of problem statements from the industry and other FIs for our Alpha Startups: MyFintech Week. Listed below are the problem statements deconstructed and summarised:

Banking

Throughout the world, one of the fintech vertical being disrupted the most has been the banking industry, particularly lending. Not only is trust in banks plummeting, with trust in tech companies such as Amazon and Google being almost at the same level of banks, newer, better, and much more customer-centric solutions are popping up.

Throughout the world, one of the fintech vertical being disrupted the most has been the banking industry, particularly lending. Not only is trust in banks plummeting, with trust in tech companies such as Amazon and Google being almost at the same level of banks, newer, better, and much more customer-centric solutions are popping up.

With the rise of Neo and Challenger banks, banks are facing much more pressure to innovate. Neo-banks are stealing market share from existing banking customers, and even the unbanked population, through their innovative functions, intuitive design, and unparalleled customer experience.

With that in mind, the problem statements for the Alpha Startups: MyFintech Week revolves around the current customer pain points. With the rise of technology and the shift in customer behavior, digital banking solutions are one of the biggest pain points. How can one leverage off technology to provide unparalleled customer experience in a period where customers demand to be serviced anytime, anywhere?

It is oxymoronic that in the 21st century, with so much unconventional data points that collect customer behaviors, financial institutions are still yet relying on traditional, incomprehensive data sets to prove the credit worthiness of an individual. How can one utilize these unconventional data sets to provide a holistic view of an individual to devise an improved credit score?

Some successful startups in this industry consist of Monzo, valued at $1.5 billion, Revolut, valued at $1.7 billion, and Mint.com, acquired for $170 million. (I’ve linked some nice reads on these success stories; you’re welcome!)

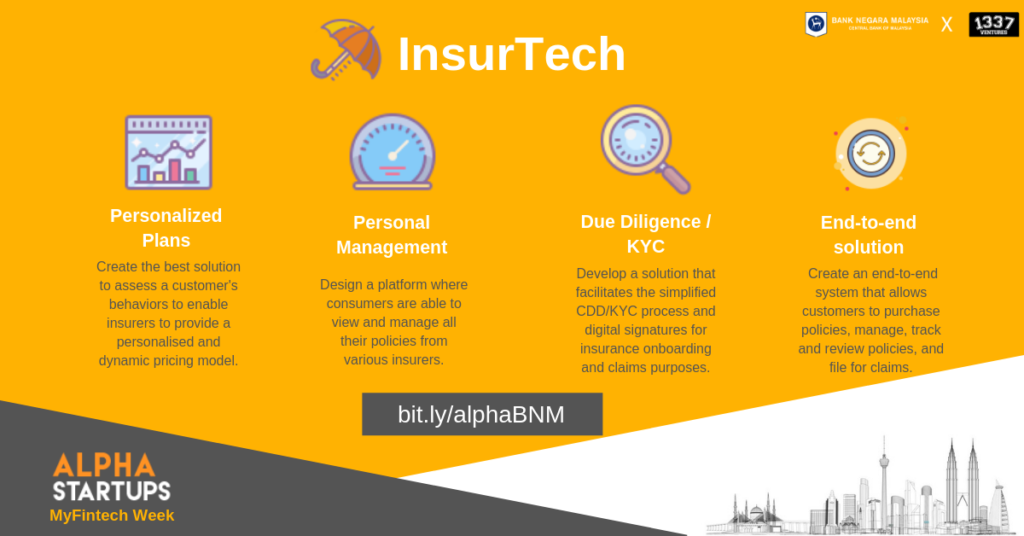

InsurTech

Insurance has remained much the same for many years and, due to a risk-averse culture, particularly resistant to change. Before the advent of new technologies, it wasn’t a competitive market where new players could easily enter. That’s all changing.

Insurance has remained much the same for many years and, due to a risk-averse culture, particularly resistant to change. Before the advent of new technologies, it wasn’t a competitive market where new players could easily enter. That’s all changing.

Just as how banking has been disrupted by new technology companies, Insurance has now become ripe for disruption by insurtech. Globally, Insurtech is growing at a CAGR of 16%, and just in Q1 2018, InsurTech startups raised nearly $1.2B.

Due to the shift in customer behavior to a much more instant gratification approach, insurance’s once “one size fits all” packages have been starting to fall out of trend. How can one design a personalised insurance package that caters to an individual’s needs and wants, producing a dynamic pricing model?

InsurTech is becoming the next big buzz word in the Fintech industry, and each day, new startups are popping up with new success stories, with some of the biggest being Lemonade that is valued at $2 billion for reversing the traditional insurance model, and Root Insurance, valued at $1 billion, that helps good drivers save money!

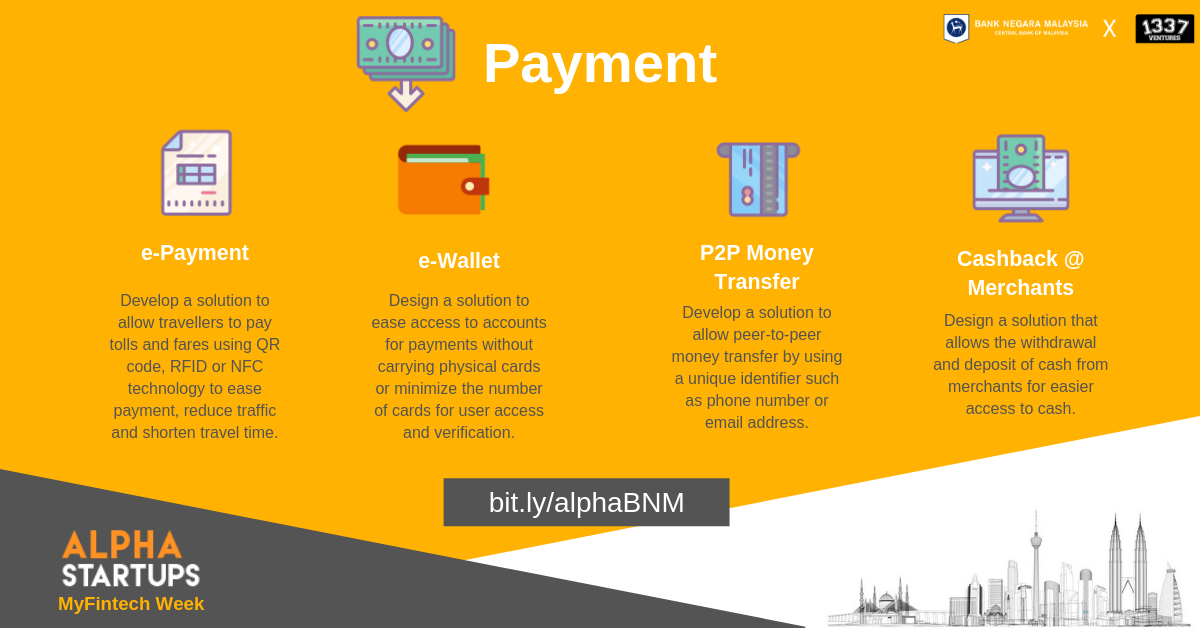

Payment

The Payment vertical is currently the most competitive one in Malaysia, with payments and wallets being the two largest representation in the Malaysian Fintech Scene (source: FintechNews.my) , standing at 19% and 17% respectively.

The Payment vertical is currently the most competitive one in Malaysia, with payments and wallets being the two largest representation in the Malaysian Fintech Scene (source: FintechNews.my) , standing at 19% and 17% respectively.

However, though representation is at large, there are still many pain points unaddressed in the market, ranging for easier payment solutions, or a unique identifier to speed up transfer process.

Though the trend towards digital payment is rising, it is difficult to see a totally cashless Malaysia in a short period of time. How can we create a solution that allows the user to withdraw and deposit money via alternative methods, as ATM queues tend to be a turn off to customers?

The transaction volume of payments in 2017 alone is at least RM 6.8 trillion. Some success stories around this field is Stripe, valued at $20 billion, and Square, valued at $32 billion.

Regtech

Regtech (Regulatory Technology) refers to technological solutions that streamline and improve regulatory processes. On the flipside, regulators are looking to utilize technology to monitor and enhance their capacity to cater not only to the rising amount of transactions, but to also parse the increasing amount of data points available in this day and age.

Regtech (Regulatory Technology) refers to technological solutions that streamline and improve regulatory processes. On the flipside, regulators are looking to utilize technology to monitor and enhance their capacity to cater not only to the rising amount of transactions, but to also parse the increasing amount of data points available in this day and age.

Invoice duplication and fraud cases in invoice financing can be mitigated by creating a database leveraging on a unique ID for each invoice/document. As for compliance checking, we’re looking for individuals to create a digital platform to help FIs perfom compliance checks and assist central banks to perform capital adequacy checks on each bank. Explore the possibility of features that facilitate exchange of digital signatures and document authentication.

Between 2015 to June 2017 itself, a total of RM115.8 million in fines and penalties were imposed on institutions for breaching our regulations and affecting the integrity of the financial system. (source: New Straits Times).

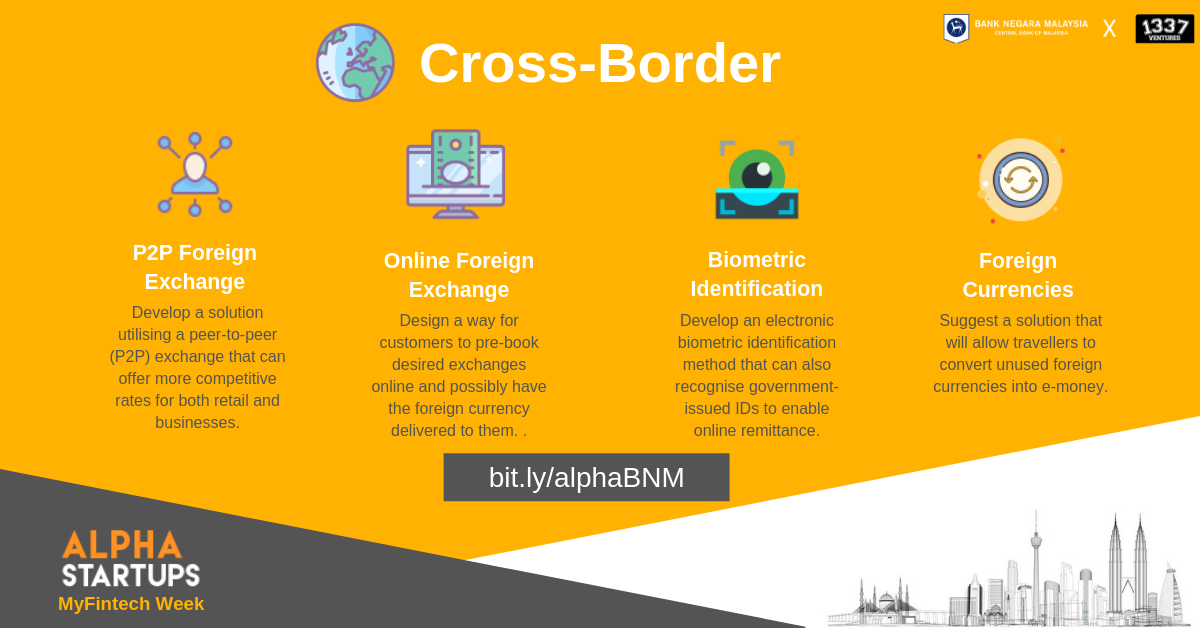

Cross-border

Though there are existing solutions in the cross-border space, there still are pain points that have yet to be relieved totally. Customers are subjected to high exchange rates when purchasing foreign currencies at money changers or any financial institution. Money changers may not have sufficient foreign currency in had to be exchanged with customers.

Though there are existing solutions in the cross-border space, there still are pain points that have yet to be relieved totally. Customers are subjected to high exchange rates when purchasing foreign currencies at money changers or any financial institution. Money changers may not have sufficient foreign currency in had to be exchanged with customers.

Currently, customers are still required to perform face-to-face verification to access remittance services. Furthermore, travellers who do not spend all their foreign currency (in cash) find it difficult to exchange it for their home currency. This is especially true for small denominations and coins.